Zurich Futura Disadvantages – 8 points to Know Before You Buy!

Is Zurich Futura the best life insurance plan in the UAE?

For many expats, it is.

But that doesn’t mean it’s right for everyone.

If you’re evaluating Zurich Futura, this guide gives you a real-world, balanced perspective based on industry data, client experience, and expert advice.

📌 Spoiler: It’s not a bad plan — but it’s often misunderstood, misused, or misaligned with the buyer’s actual needs.

Let’s explore Zurich Futura Disadvantages (and some powerful benefits) so you can make an informed decision.

1. Premiums Are Higher Than Term Plans

Zurich Futura is a whole-life policy with built-in savings. The premiums are typically higher than term insurance. (Can go upto 2 – 4 times)

However, it’s important to understand the difference between cost and price.

In the short run, Futura can be expensive because you’re paying for long-term protection and funding the establishment of a plan with investment components. These upfront costs don’t immediately build value.

But here’s where it gets interesting:

The cost of insurance gradually decreases over time due to the “sum at risk” concept.

In layman’s terms: Zurich only needs to insure the difference between your chosen life cover and the policy’s account value. As your investment portion grows, Zurich’s risk reduces — and so do your insurance costs.

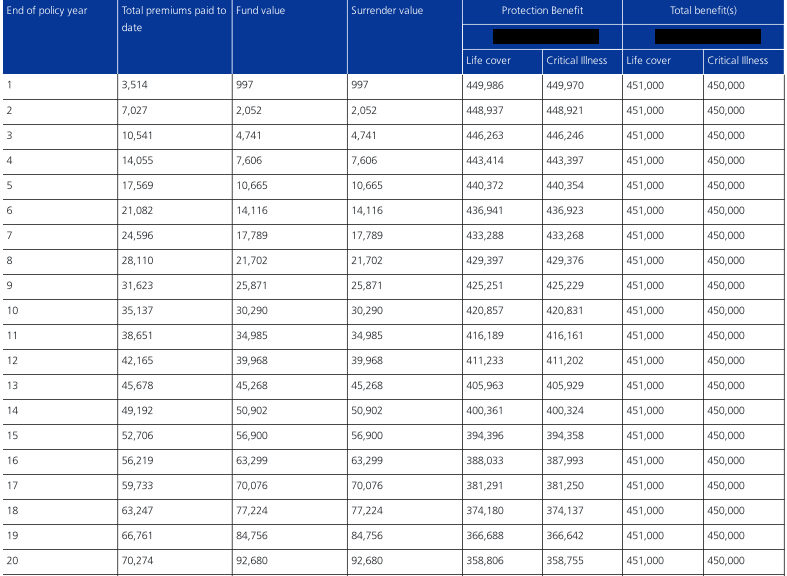

Let’s illustrate with an example:

In the screenshot below

- At the end of Year 1, the fund value is just $997, and Zurich’s liability is almost the entire life cover ($450,000). So the mortality charges are calculated on $450K less $997

- By Year 10, the fund value grows to $30,920, reducing the “sum at risk” to ~$419,000. Then the mortality charges are only levied for ~$419,000.

- By Year 20, the fund is worth $92,680. Now Zurich only insures the gap (~$357,000).

So while the price seems high initially, the true cost of keeping the policy can become much lower over time — especially if the plan is structured well.

A good advisor can customize the premium, benefits, and riders to fit your needs and budget, making the policy cost-efficient over 20+ years.

But Isn’t Term Insurance Always Better?

Term Insurance is no doubt efficient and affordable.

You may find many Finfluencers on the internet swearing that Term Insurance is always better.

And they would be right — in countries with robust social security systems, mandatory pensions, and universal healthcare.

For example, in India, the mandatory contribution to EPF by the employer and employee is 12% each. That means 24% of one’s salary is invested in a safe, compounding fund for decades — creating substantial retirement security.

But in the UAE, most expats do not have such safety nets:

- Employer medical insurance ends with employment

- Pension plans are rare

- There is no state-provided post-retirement income

In this context, Zurich Futura offers the best of both worlds:

- Comprehensive whole life cover

- Living benefits like critical illness and disability

- Long-term savings that build cash value over time

When you no longer need the insurance, you can surrender the policy and withdraw the accumulated value.

Futura isn’t just about protection — it fills the retirement and security gap left by the lack of government and employer-backed benefits in the UAE.

Also, many expats face a harsh reality with their health insurance. If you make a large claim, the next year’s premium often shoots up — and stays high. This makes ongoing coverage unaffordable for many.

💡 A critical illness rider under Zurich Futura can offer a much-needed buffer in these cases.

2. It’s a Long-Term Commitment

Futura is best suited for people who require long-term cover and are Not looking for a short term investment plan. Early withdrawals or surrender may result in losses due to setup charges and low accumulated value in the initial years.

If your income is uncertain, or if you have plans to leave the UAE and discontinue premiums early, this plan may not be ideal.

3. Misunderstood as an Investment Product

Zurich Futura is insurance-first, investment-second. It’s designed to provide lifelong protection, not short-term investment returns.

Many clients expect it to behave like a mutual fund, but the investment portion is meant to support the insurance over the long term — not to outperform markets.

This plan can be oversimplified at the time of sale — especially by those looking to sell to clients who want to buy an investment plan.

4. Charges Are Front-Loaded — Growth Is Gradual

Zurich Futura has transparent and clearly defined charges that apply throughout the policy:

- Establishment Charges:

- 50% of each premium in Years 1 & 2

- 7% in Years 3–5

- 2% annually from Year 6 onward

- Monthly Admin Fee: ~$7.50 per month

- Cost of Insurance (COI): Varies by age, coverage, and investment value

- Rider Charges: For optional benefits like CI, disability, income replacement, waiver of premium, etc.

In term insurance, 100% of your premium is a charge — it provides pure protection, but no value is built. The cost is hidden.

In Futura, you see the charges, and if designed right, part of your premium builds value while offering lifelong benefits.

Both types of insurance have costs. But Futura makes the costs visible — and offers flexibility, investment access, and value creation over time.

5. Perceived Rigidity

Earlier versions of Futura had 0% allocation in the first two years. That changed post-2020.

Today’s version offers:

- 50% allocation even in the first two years

- Ability to pause premiums (if account value permits)

- Options to reduce cover, add/remove riders, and adjust premiums

Still, it’s not a short-term plan. Surrendering early can impact value.

6. Upgrade Limitations After Relocation

Once you leave the UAE, applying for increased cover or new riders might be restricted based on where you move and local regulations.

That said, your policy continues as long as you follow the terms. This restriction also applies to all types of policies in the UAE.

7. Clients Often Don’t Ask the Right Questions

This plan can be oversimplified at the time of sale — especially by those looking to sell to clients who want to buy an investment plan.

Many clients:

- Don’t fully review their proposal

- Overestimate the investment element

- Ignore how long the policy actually runs (beyond the premium payment term)

- Don’t ask how charges affect performance

- Don’t monitor or rebalance fund performance regularly

As a result, they may walk in with wrong expectations and walk out disappointed — not because the plan failed, but because the right questions were never asked at the beginning.

A good advisor will walk you through all these elements upfront, ensuring you know what you’re signing up for — and what to expect over time.

8. Break-Even Happens Late (Year 13–14)

If you pay premiums for 15 years, you’ll likely break even around Year 13 or 14.

This depends on:

- Age at entry

- Type and cost of riders

- Actual fund returns vs projected

Futura is not ideal if you plan to surrender early or expect quick liquidity.

Unique aspects of Futura.

Fixed Income Term Rider: A Game-Changing Option

This affordable rider offers monthly payouts to your family in the event of your death. Think of it as a second salary — a great tool for families with young children or financial dependents.

Comprehensive Critical Illness and Living Benefits

Zurich Futura offers optional riders like:

- Critical Illness (35 conditions + child cover)

- Permanent and Total Disability

- Cancer-only Cover (lower cost)

- Accidental Death, Hospitalization

- Waiver of Premium

These riders turn your policy into a complete protection plan.

Efficient Claims Support

Zurich paid $241 million in claims across the Middle East.

- 98% of life claims settled

- Payout within 72 hours once documents are in

That’s the kind of reliability you want from your insurer.

Is Zurich Futura Right for You?

It could be — if you:

- Are under 45

- Want long-term life cover (20+ years)

- Prefer building value instead of paying for pure term

- Want optional living benefits like CI, disability, or family income

- Don’t plan to liquidate the policy early

- Are willing to structure it with expert guidance

Final Thoughts

Zurich Futura has its downsides — especially if misunderstood, misused or mis-sold

But when structured properly, it becomes more than a policy. It becomes:

✅ A smart protection strategy

✅ A backup capital accumulation strategy

✅ A flexible tool for wealth transfer

📞 Book a Discovery Call to assess if Zurich Futura is the right long-term protection strategy for you.

Click here to book a Discovery Call.

Author, Blogger & Independent Financial Advisor. My goal is to give you actionable tools for creating passive income and building wealth. More than 10,000 expats have already used my ideas to jumpstart their journey towards financial independence. Connect with me to start yours…