Critical Illness Insurance in UAE: Cover, List & Costs (2026 Guide)

Life can take unexpected turns. One moment, everything seems fine, and the next, a critical illness could disrupt your health, income, and long-term financial plans.

For expats in the UAE, this situation can be even more challenging. Losing your ability to work doesn’t just affect your paycheck. It can also mean losing your employer-provided medical insurance, visa sponsorship, and other benefits, leaving you and your family vulnerable. And even if you hold a golden visa, so your residency is secure, managing rent, school fees and everyday expenses here without an income coming in is a struggle very few families can sustain for long.

This is where critical illness insurance makes all the difference. By providing a lump sum payout upon diagnosis of a covered condition, it ensures you can:

- Focus on recovery without financial stress.

- Cover essential expenses like rent, school fees, and medical costs.

- Protect your family’s future from uncertainty.

Table of Contents

What is Critical Illness Insurance?

It is a protection policy that pays you a cash lump sum if you are diagnosed with a serious illness covered by the policy, such as cancer, a heart attack or a stroke. The money is yours to use however you like, whether that’s treatment, rent, school fees or simply replacing your salary while you recover.

Why it is important?

When an expat in the UAE can’t work, the salary isn’t the only thing that stops. Three things tend to go at once.

- The medical insurance, because it’s usually tied to your job, so suddenly treatment is out of pocket.

- The visa sponsorship, which puts your right to stay in the country in question.

- The allowances for housing and schooling, which end with the salary.

A lump sum payout doesn’t ask whether you still have a job or a sponsor. It just lands in your account when you need it most. In a market where so much of your life is tied to your employment contract, that independence is crucial.

Critical Illness Insurance List: Conditions Covered

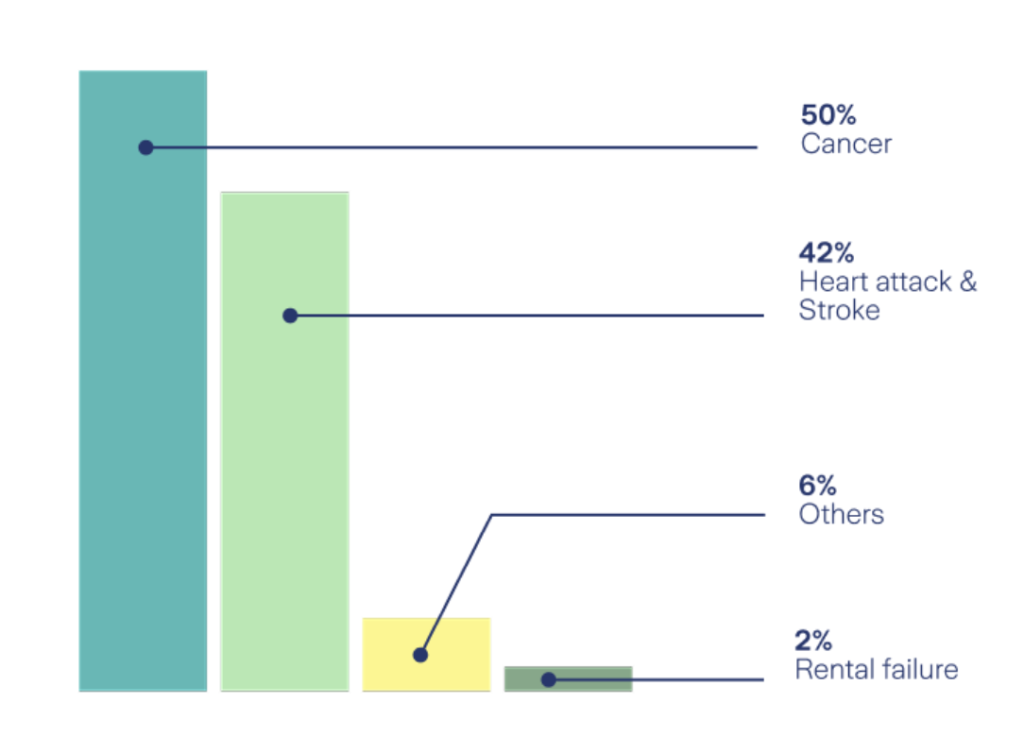

Every insurer’s list is slightly different, but a good policy in the UAE will cover the conditions below. The three big ones, cancer, heart attack and stroke, account for the vast majority of all claims paid.

- Cancer: most invasive cancers (around 48% of claims globally)

- Heart & circulatory: heart attack, stroke, coronary bypass, heart valve surgery (around 44% of claims)

- Organ failure: kidney failure, major organ transplant, liver failure

- Neurological: multiple sclerosis, Parkinson’s, motor neurone disease, benign brain tumour

- Other major: major burns, loss of sight, hearing or speech, paralysis, coma

Here’s the part most people skip: the exact wording matters enormously. Two insurers can both say they cover “cancer” and define it completely differently. Reading those definitions properly before you sign is exactly the sort of thing I do with clients, because it’s where claims are won or lost.

How Much Does Critical Illness Insurance Cost in the UAE?

There’s no flat price. Your premium comes down to four things:

- Your age. This is the big one, and it climbs every year you wait.

- Your health and lifestyle, including medical history and whether you smoke.

- The sum assured, meaning how big a payout you want.

- The structure, standalone or as a rider on life cover.

Premiums can start as low as around AED 200 a month. The honest takeaway, though, is that the cheapest policy you’ll ever be offered is the one you take today. Buy young and healthy and you lock in a low rate for decades. Wait until your 40s or 50s and the same cover costs far more, assuming a new diagnosis hasn’t priced you out altogether. Get a quote for your own numbers here.

Standalone Critical Illness Insurance vs. Rider

Standalone critical illness cover This is a dedicated policy, independent of anything else, and you can shape it around your own needs. It’s the right call if you want focused protection you’re in full control of.

A rider on your life insurance Bolt it onto term life and you get affordable protection through the years when your responsibilities are highest, like the mortgage and the kids’ schooling. Bolt it onto whole life and you get lifelong cover that also builds some cash value along the way.

How much cover should you take?

As a starting point I tell clients to aim for three to five years of annual income, which keeps the household running while you recover. On top of that, add enough to clear the big liabilities, typically the mortgage or whatever’s left of the children’s education. If you’re not sure what your number should be, that’s a five-minute conversation, not a guess.

Who Needs Critical Illness Insurance?

Honestly, almost anyone earning an income or carrying responsibilities. But a few groups feel the benefit most:

- Young professionals, who can lock in the lowest premiums before any health issues show up.

- Families with children, where one illness shouldn’t derail the school fees.

- Expats leaning on employer benefits, who’d lose the medical cover and the visa with the job.

- Single breadwinners, whose family has no second income to fall back on.

- NRIs supporting family back home, who need cover that keeps the EMIs and the support going even after they leave the UAE.

- Pre-retirees and retirees, who’d otherwise have to raid the retirement pot to pay for a diagnosis.

The cost of waiting

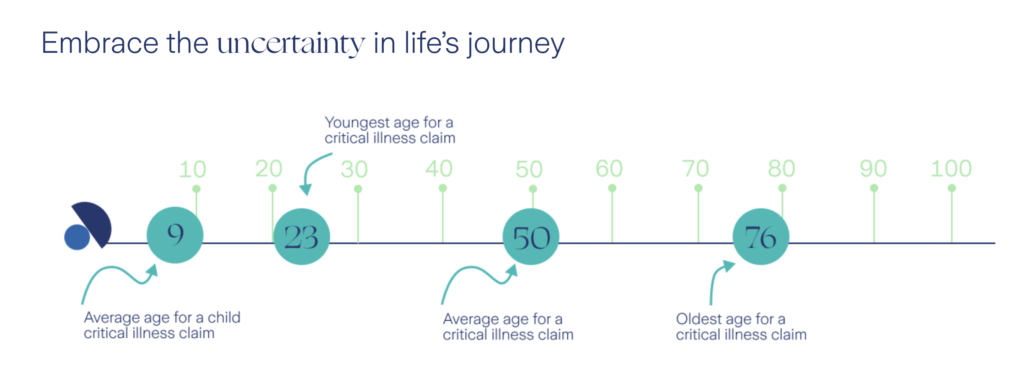

Delay works against you twice over. The premium goes up every year, and any new health condition can make cover dearer or simply unavailable. The average claim is made around age 50, which tells you the cover needs to already be in place well before then to be worth anything.

Three myths worth clearing up

“I’m young, I don’t need it yet.” The youngest critical illness claim recorded in the UAE was someone aged 23. Being young lowers your premium. It doesn’t lower your risk to zero.

“My health insurance has it covered.” Health insurance pays the hospital. It won’t replace your salary or cover the rent, the school fees or the childcare.

“I’ll just dip into savings.” A serious illness can run into hundreds of thousands of dirhams over a couple of years, long enough to undo a decade of saving.

Don’t wait for a diagnosis to find out you’re underinsured

The best time to sort this out is while you’re healthy and your premiums are low, because that window doesn’t stay open. In a free 30-minute call I’ll show you exactly what a serious illness would cost your family, what your employer cover does and doesn’t protect, and the right level of cover for your situation. No jargon, no pressure.

Book Your Free Discovery CallDon’t wait for a diagnosis to find out you are Uninsured or underinsured

The best time to sort this out is while you are healthy and your premiums are low, because that window doesn’t stay open for long for most.

In a free 30-minute call I’ll show you exactly how a serious illness could disrupt your families finances, what your employer cover does and doesn’t protect, and the right level of cover for your situation. No jargon, no pressure.

Frequently Asked Questions

How much is critical illness insurance in the UAE?

The cost depends on factors such as:

Your age, health condition and lifestyle.

The amount of coverage you choose.

Whether it’s a standalone policy or a rider on life insurance. Premiums can start as low as AED 200 per month.

Is it worth getting critical illness insurance?

Yes, critical illness insurance is worth it, especially for expats in the UAE. It provides a safety net during your most vulnerable times, ensuring financial stability when you may lose your job, medical insurance, and visa sponsorship due to a serious illness. Learn more: Is Critical Illness Insurance Worth It?

How is critical illness insurance different from medical insurance?

Medical insurance covers the cost of hospital treatments, doctor consultations, surgeries, and medications. It’s designed to handle immediate medical expenses. Critical illness insurance provides a lump sum payout upon diagnosis of a covered serious illness. This payout isn’t restricted to medical bills. You can use it for:

– Replacing lost income during recovery.

– Paying rent, school fees, or other daily expenses.

– Covering alternative treatments or rehabilitation costs.

In short, medical insurance keeps you covered in the hospital, while critical illness insurance keeps you financially stable outside it.

What are the disadvantages of critical illness insurance?

It offers real benefits, but there are limitations worth knowing:

– Waiting periods: most policies have a 90-day waiting period.

– Exclusions: pre-existing conditions are excluded or priced at a higher premium.

– It doesn’t cover self-inflicted injuries.

– Maximum entry age is 59 for certain types of policies.

Why would critical illness insurance not pay out?

A claim may not be paid if:

– The diagnosis doesn’t meet the policy’s specific definition of the illness.

– The illness occurs during the waiting period.

– The claim is for a pre-existing condition not covered by the policy.

– Incomplete or incorrect documentation is submitted during the application or claims process.

– The claim is due to a self-inflicted injury, or active participation in war or illegal activity.

Can I continue my critical illness insurance plan if I move out of the UAE?

Yes, in most cases you can keep your policy even if you relocate.

Many international insurers offer global coverage, so it stays valid wherever you live, as long as you keep paying the premiums. That said, it’s worth doing three things:

– Check the terms of your policy to confirm there are no restrictions tied to a change of residency.

– Inform your insurer about the move so they can update your records.

– Review the currency implications. If your policy is in AED, a move abroad may mean converting currency to pay premiums.

For a smooth transition, talk to your financial advisor before buying or relocating.

Is there an age limit for purchasing critical illness insurance?

Most insurers set an entry age limit, usually somewhere between 18 and 59. Cover then typically ends at a set age such as 75 or 80, depending on the policy.

Can I buy critical illness insurance if I have pre-existing conditions?

Yes, you can, though pre-existing conditions may either:

Be excluded from coverage, or

Increase your premiums. Disclose your full medical history when you apply. Leaving things out is the fastest way to have a claim rejected later.

Should I get critical illness or life insurance?

It depends on what you’re trying to protect:

Critical illness insurance protects you during your lifetime, covering recovery costs and lost income.

Life insurance looks after your loved ones after you’re gone. Plenty of people take a life insurance policy with a critical illness rider, which is a cost-effective way to get both. More on combining the two: What is Critical Illness Insurance?

Critical illness cover in India or the UAE, which is better?

Indian insurers have started offering critical illness cover fairly recently, with sums assured up to around USD 100,000. The premium is roughly the same, but the scope is much wider in the UAE, and setting up a policy and making a claim is far more seamless here. There are two extra catches with the India route. India charges 18% GST on term insurance plans, which pushes the cost up, and rupee depreciation steadily erodes the real value of an INR policy over time.

Book a free discovery call

I’m an independent financial advisor in Dubai, and I’ve spent years helping expat families pick cover that fits their actual situation rather than whatever happens to be on sale. On a quick call we’ll look at what you already have, work out whether a standalone policy or a rider makes more sense, and settle on a plan that lines up with your goals.