-2.png?width=750&height=750&name=A%20goal%20properly%20set%20is%20halfway%20reached.%20-%20(750%20%C3%97%20750%20px)-2.png)

Financial Wellbeing, 30 Days Challenge, Win with Money,

30 Days Win With Money Challenge

The last three years were challenging on multiple fronts, and money was one of them for many of us.

If you are on 100% variable income, there is no upper limit to how much money you can make, but there is never a minimum income guarantee also.

The feast or famine cycle is typical for freelancers, Real estate Agents, salespeople on commission only, and emerging entrepreneurs/professionals.

Additionally, if you do not hold traditional benefits, such as comprehensive health insurance, group life insurance, and retirement plans. This can make it more difficult to protect yourself financially in the event of an emergency.

Planning and investing for your financial future in such circumstances can be a challenge.

However, you can navigate this situation successfully with careful planning and intelligent decision-making.

Here are five financial planning tips to help you:

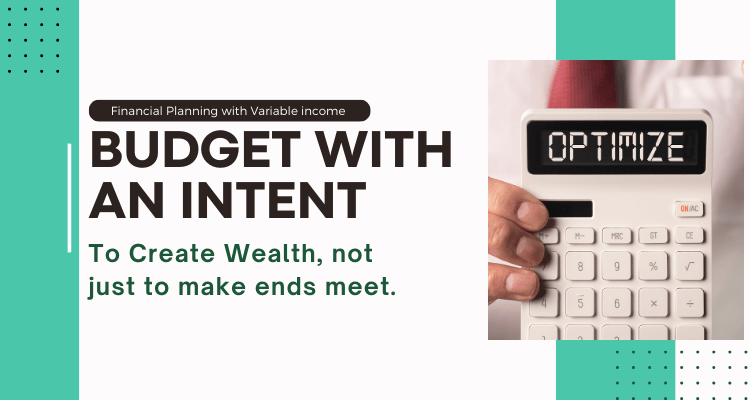

The purpose of a budget is not just to make ends meet. Its purpose is to help you do more with your money. It should help you optimize your income and expenses to increase your savings and accumulate wealth.

Budget with the intent to generate a surplus every month for saving and investing.

Read this insightful article from YNAB to learn how to budget on a variable income.

"A goal properly set is halfway reached." - Zig Ziglar.

While Goal setting seems basic and obvious, you will be surprised that many do not have empowering goals.

They don't set goals because they let their past experiences create doubts and uncertainty about being able to set and achieve goals.

They stay in a comfort zone, doing just enough to make just enough money.

Please remember that your Past is not equal to the Future.

Create a Financial Plan with powerful and motivating goals for short, medium, and long terms. Make them visual, create a vision board, and place it where you can see it daily.

Mark shorter milestones. Celebrate reaching significant milestones and stay consistent with your efforts.

People with variable incomes are often so focused on the present that they neglect their future.

They may live paycheck to paycheck, struggling to make ends meet, often ignoring long-term goals like retirement, emergency savings, or their children's education.

The challenge is that this situation often continues into the future, and they remain stuck in the rat race.

The easiest way to break this trend is to pay yourself first strategy. Start small and set aside a fixed percentage of your income/revenue for your future goals every time you get paid.

Click here to read more about the Pay Yourself First Strategy.

Everyone should have an emergency fund. But if you are on variable income, you need more;

Set up two separate accounts for

The Emergency Savings account should cover at least six months of expenses to help you manage emergencies and longer income gaps.

The Expense Buffer account is like a working capital fund for your personal expenses. It helps you operate seamlessly and focus on your expenses and long-term financial goals.

Ideally, you should have three months of expenses in this account to give you a sense of certainty.

Once you have funded the emergency fund and expense buffer accounts, you can start investing for the future.

Investing is making your money work for you.

There are many different types of investments; click here to read about the Best investment options in UAE for short, medium, and long-term goals.

Managing your finances with a variable income can be challenging, but you can break free from the Rat Race and achieve Financial Freedom by following the above tips.

Seek professional help to create a Holistic Financial Plan, stay on course, and reach your goals faster.

Click here to schedule a Free Consultation.

The last three years were challenging on multiple fronts, and money was one of them for many of us.

-2.png?width=300&name=How%20do%20you%20feel%20(350%20%C3%97%20250%20px)-2.png)

Don't you hate it when you miss an exit twice on E311 or on Sheik Zayed road?

No one wants to die early, but the sad truth of life is that people die sooner or later.