6 Reasons To Use Regular Savings Plan To Build Wealth In UAE.

For many, including you and me, the opportunity to build wealth and secure financial independence is perhaps the key motivator for being an expat.

The UAE’s strong economy and tax-free income offer us a fair chance to achieve these goals.

However, a high income doesn’t automatically lead to lasting wealth. Without a disciplined approach to saving and investing, it’s easy to remain “rich by income but poor in wealth.” Many enjoy a luxurious lifestyle but have little to show in terms of net worth and long-term financial security.

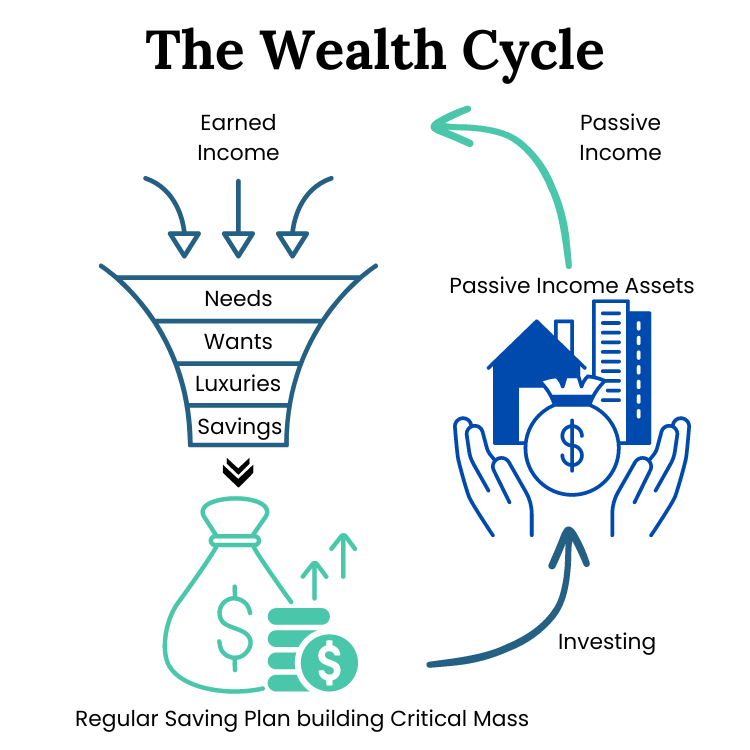

One of the most effective tools for long-term wealth accumulation is a regular savings plan or SIP – Systematic Investment Plan.

Here are Six reasons why you should consider using a regular savings plan or SIP to build wealth and take advantage of future opportunities.

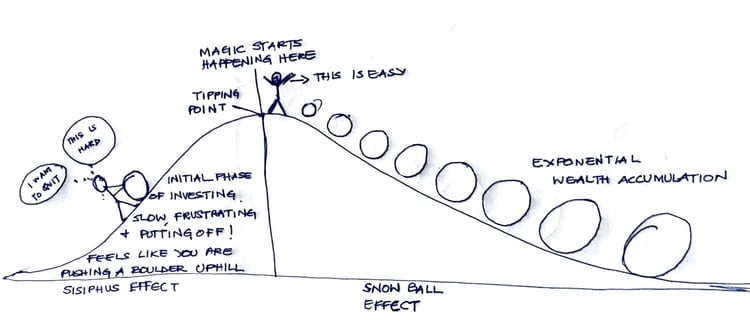

1. It Gets You to the Tipping Point

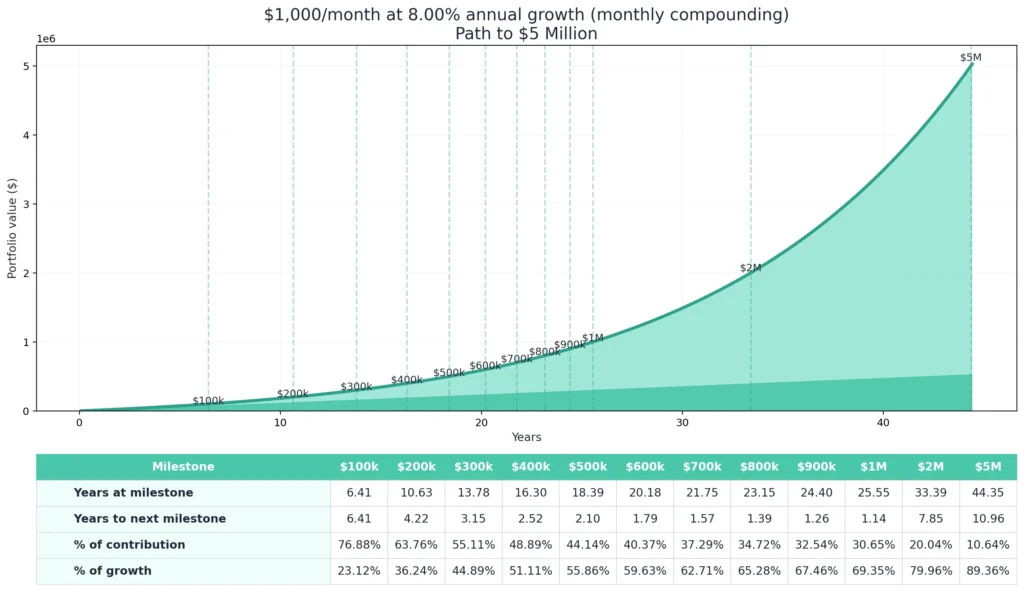

Many say the first $100,000 or the first million is the most difficult to accumulate and that is very true!

This is because the initial stage of wealth building requires both discipline and patience, and the returns often feel slow and low. The real challenge lies in reaching the tipping point where your savings begin to work significantly in your favor, and your money starts growing faster than your contributions.

A medium to long-term regular savings plan/SIP is the easiest and most efficient way to convert your surplus income into wealth. It helps you put away small sums of money every month, that grow and increase in value over time.

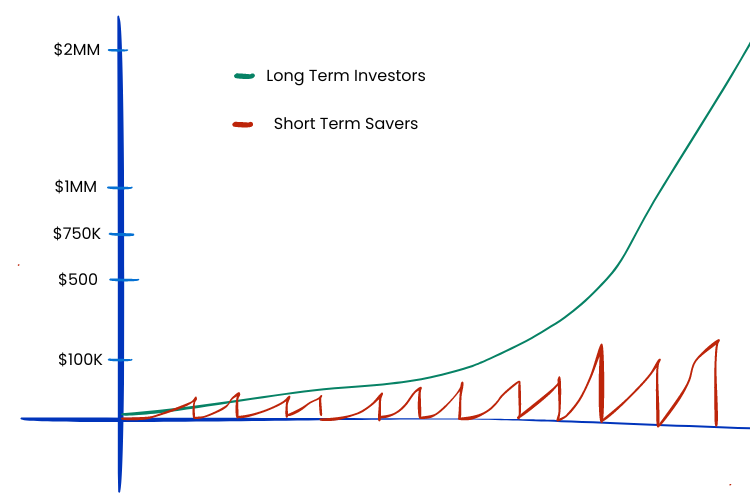

However, the challenge for many expats is that they tend to be short-term savers. While it may seem like they’re saving every month, they never quite reach the tipping point because they often withdraw their funds for short-term expenses or small investments that aren’t substantial enough to tip the scales. This prevents their savings from compounding and growing into the critical mass needed to generate meaningful wealth.

Additionally, it’s not just about achieving high returns—it’s about building enough capital. For example, even if you achieve a 30% annual growth rate on an investment of $20,000, it will still take time before you see meaningful results. However, once you’ve reached a critical mass of savings, even moderate returns of 8-10% can generate substantial wealth over the next 10 to 15 years.

A regular savings plan ensures that you’re steadily building this critical mass, allowing you to benefit from both high-growth opportunities during favorable market conditions and steady, consistent returns over the long term. Once you hit that wealth tipping point, your financial growth accelerates in ways that truly make a difference.

2. Take Advantage of Wealth-Catapulting Opportunities

Throughout your lifetime, you may encounter several major opportunities that have the potential to rocket power your wealth to the next level. The key to taking advantage on these opportunities lies in being financially prepared to act on them when they arise.

Example: The Recent AI Boom

The recent surge in Artificial Intelligence (AI) and machine learning technologies has created massive investment opportunities. Companies specializing in AI have seen exponential growth, and early investors have reaped substantial returns. For instance, investments in AI-driven companies and technologies have outperformed traditional markets, offering significant wealth-building potential.

Those who recognized the potential of AI early on and had the liquid capital to invest were able to capitalize on this boom, substantially increasing their wealth. This underscores the importance of being financially prepared to seize such opportunities.

The irony is that this opportunity rose in late 2022 and early 2023, when the global markets were down in the wake of high interest rates and inflation.

Many opportunities in the past have risen amidst chaos and uncertainty, making it more difficult to spot them.

Past Opportunities

Other historical examples include:

- The Dot-Com Boom and Bubble (late 1990s to early 2000s): This decade began with the gulf war and ended with the Y2K and the Dot com bubble Despite all this chaos there were tons of opportunity and smart investors who had the liquidity and awareness were able to spot the opportunity and scale their wealth.

- The Global Financial Crisis (2008-2009): The market downturn presented opportunities to invest in undervalued assets, leading to significant gains during the recovery.

- The Rise of Cryptocurrencies (2010s): Early adopters of Bitcoin and other cryptocurrencies experienced substantial wealth growth.

- COVID-19 Pandemic (2020): Market dips followed by swift recoveries in sectors like technology and healthcare offered significant investment opportunities.

Future opportunities will undoubtedly arise, but only those with available capital will be able to seize them. By regularly saving and building a liquid fund through an RSP/SIP, you position yourself to take advantage of these wealth-catapulting events.

3. Reinvesting in Passive Income-Generating Assets

Once you’ve built a substantial pool of savings through an RSP, you can begin reinvesting into passive income-generating assets such as dividend-paying stocks, bonds, real estate, or even REITs (Real Estate Investment Trusts). These assets not only provide ongoing income but also accelerate your wealth accumulation as you reinvest the earnings.

This creates a powerful snowball effect, where your capital grows faster due to compounding returns and reinvested income. Eventually, your passive income can become a key source of financial independence, allowing you to maintain your lifestyle without relying solely on active income.

For eg: You can accumulate enough money to put as a down payment on an investment property that can provide rental income and capital appreciation. If the rent can cover the mortgage and ancillary expenses, you can restart this process to buy another property…

In 15 to 20 years, you will have a portfolio of properties that are almost paid off and generating consistent passive income.

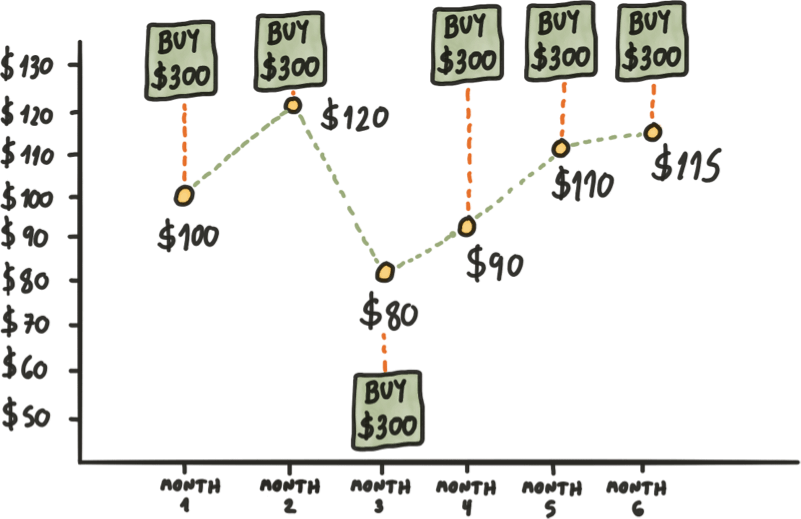

4. Benefit from Dollar Cost Averaging

Timing the market is notoriously difficult, even for seasoned investors. One of the great advantages of regular savings plans is that they utilize dollar-cost averaging. This means that you invest a fixed amount regularly, regardless of market conditions. When prices are high, you buy fewer units, and when prices are low, you buy more.

Over time, this approach smooths out the impact of market volatility, allowing you to accumulate assets at a lower average cost. This reduces the risk of poor market timing and ensures that your investment grows steadily over the long term.

Image Source: https://thetradingbible.com/

5. Tax-Free Growth

As a resident of the UAE, you benefit from a tax-free environment—which means your investments grow without being subject to capital gains tax. This advantage, combined with regular contributions, can accelerate the wealth-building process significantly. Regular Savings Plans make it easy for you to benefit from this favourable tax regime, allowing you to retain and grow more of your earnings.

If the same investing is done outside UAE, you may have to pay a certain tax depending on your residency or domicile.

|

Country |

Short-term Capital Gains (STCG) |

Long-term Capital Gains (LTCG) |

|

India |

20% for equities and other assets |

12.5% for equities and other assets |

|

USA |

Taxed as per income tax rates (10%-37%) |

0%, 15%, or 20% depending on income |

|

UK |

10%-20% depending on income level |

10% for basic rate, 20% for higher rate |

|

Pakistan |

12.5% on listed securities |

10% for other assets |

|

Bangladesh |

15% on unlisted securities |

Exempt for individual investors on listed securities |

|

Australia |

Marginal rate up to 45% |

50% exemption, remaining taxed at marginal rate |

|

France |

30% flat rate |

30% flat rate |

|

Canada |

Marginal rate up to 33% |

50% of gains taxed at the marginal rate |

|

Germany |

Flat rate of 25% + surcharge |

Flat rate of 25% + surcharge |

|

Russia |

13% for residents, 30% for non-residents |

13% for residents, 30% for non-residents |

|

China |

20% for real estate, exempt for securities |

20% for real estate, exempt for securities |

The data presented above may not be relevant due to changes in tax regimes.

6. Goal-Based Investing

Regular Savings Plans are tailored to meet specific financial goals, whether you’re saving for your children’s education, your retirement, or a large purchase like a house. With a clearly defined target, these plans keep you motivated to contribute regularly and stay on track. Some plans even come with helpful goal-tracking features, letting you monitor your progress toward achieving your objectives.

Example: You can earmark contributions for different life stages, such as buying a home, your children’s future, or a comfortable retirement.

Conclusion: Preparing for the Future

For expats in the UAE, building long-term wealth requires more than just a high income. It demands a structured, disciplined approach to saving and investing. By using a regular savings plan, you can systematically build a critical mass of wealth, take advantage of your higher disposable income and tax free capital appreciation, and set yourself up for a future of financial freedom.

Whether you want to secure your retirement, fund your children’s education, or simply be ready for the next big opportunity, an RSP is one of the most reliable ways to achieve your financial goals. So start today, build your liquid funds, and ensure that you’re prepared to capitalise on the wealth-building opportunities that come your way.